Breadth Check: Rally Or Roll Call?

This week’s breadth feels like a market that wants to trend, but keeps checking its rearview mirror. Participation is decent in the big indexes, thinner in the small caps, and the risk tone is “constructive but not yet a stampede.” New highs are trying to show up to work, but they have not filed for overtime.

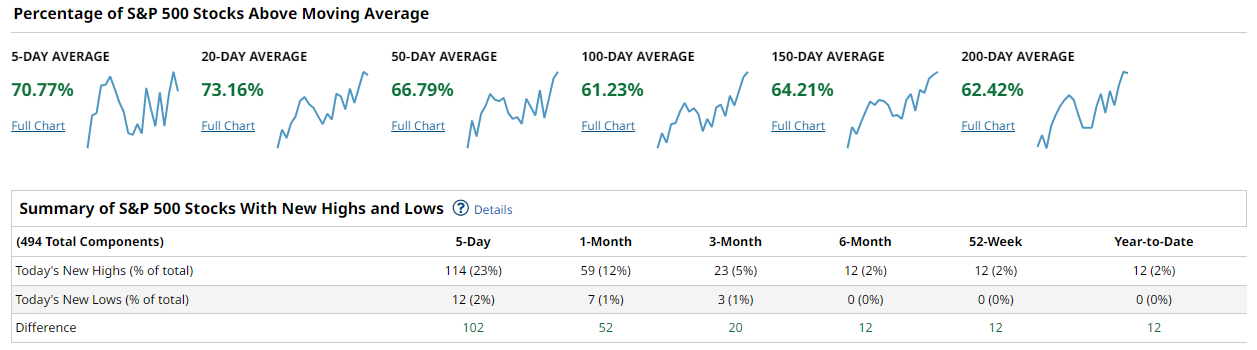

The S&P 500 still has a healthy share of members above their short and intermediate moving averages, with the 5-day and 20-day cohorts clearly stronger than the long-term 150- and 200-day buckets.

In plain English: more stocks are riding the recent uptrend than are breaking long-term downtrends, which fits a market grinding higher rather than launching in a fresh, breathless thrust. New highs are present but not dominating, and new lows have not disappeared, which argues for steady, not euphoric, risk-taking.

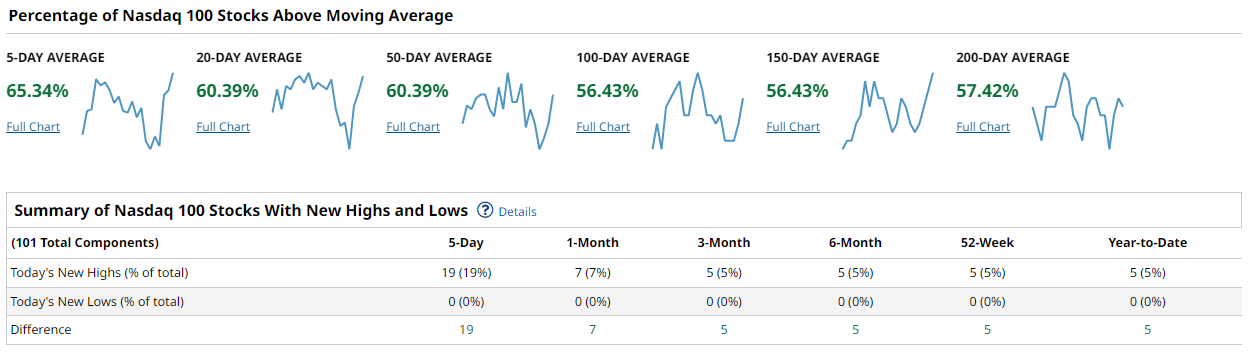

In the Nasdaq 100, the short-term breadth is firmer than you might expect given the index’s reputation for being carried by a handful of megacaps. The share of names above 5- and 20-day averages has improved from recent weeks, even as the 50- and 100-day cohorts remain only moderately aligned.

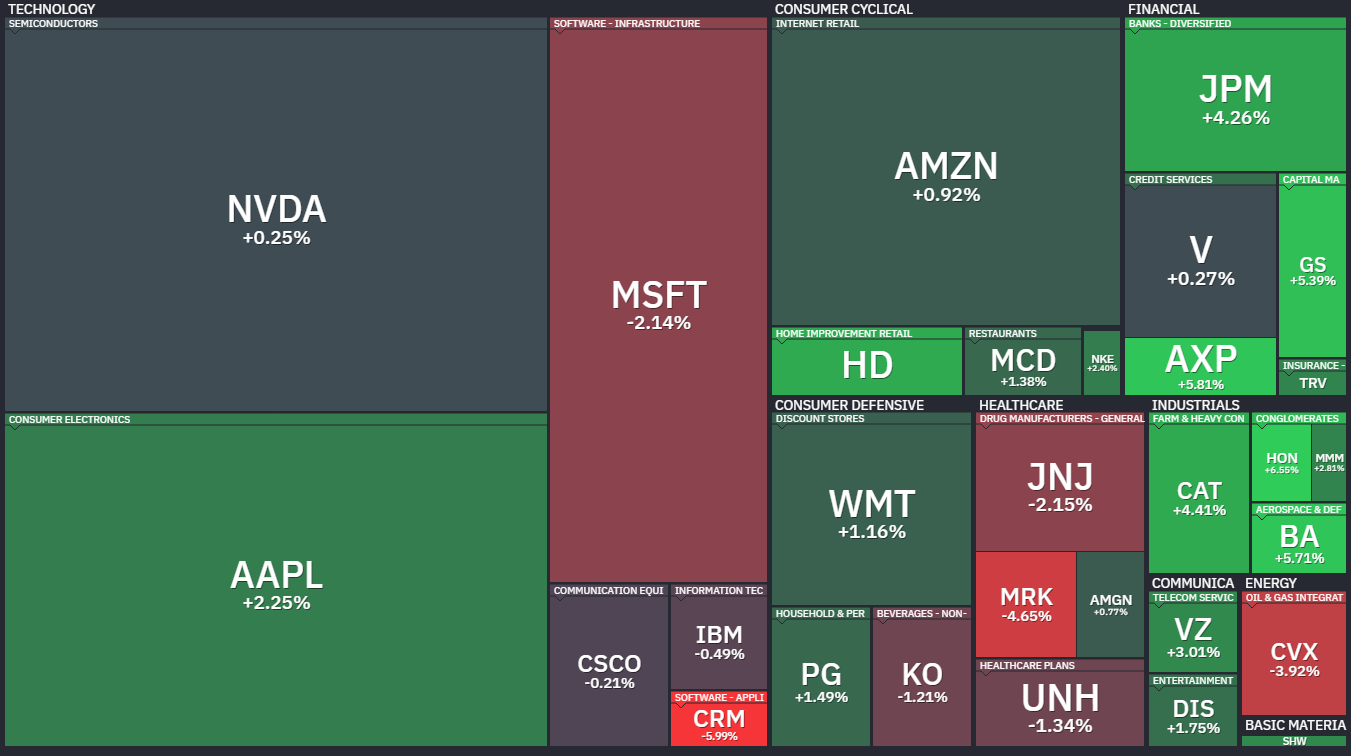

The weekly return heatmap is still very top-heavy, with the largest tech and AI names pulling most of the weight, but participation beneath the surface is “okay” rather than “only five stocks matter.”

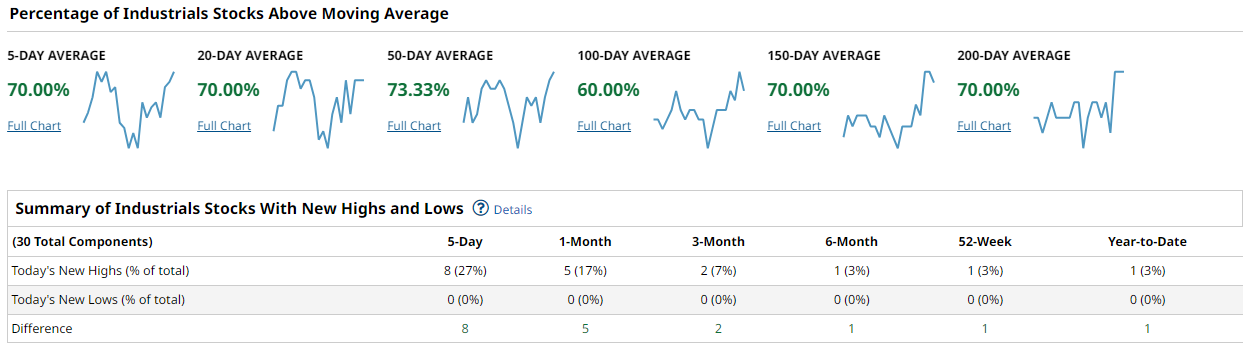

The Dow’s breadth sits somewhere between “boomer comfort” and “tactical opportunity.” A reasonable fraction of Industrials components are above their key trend filters, but the longer-dated moving-average cohorts lag the S&P, reflecting a more uneven leadership mix.

New highs are there, but Dow constituents are not exactly stampeding into blue-sky territory, so the index functions more as a confirmation of risk-on than as the spearhead of the move.

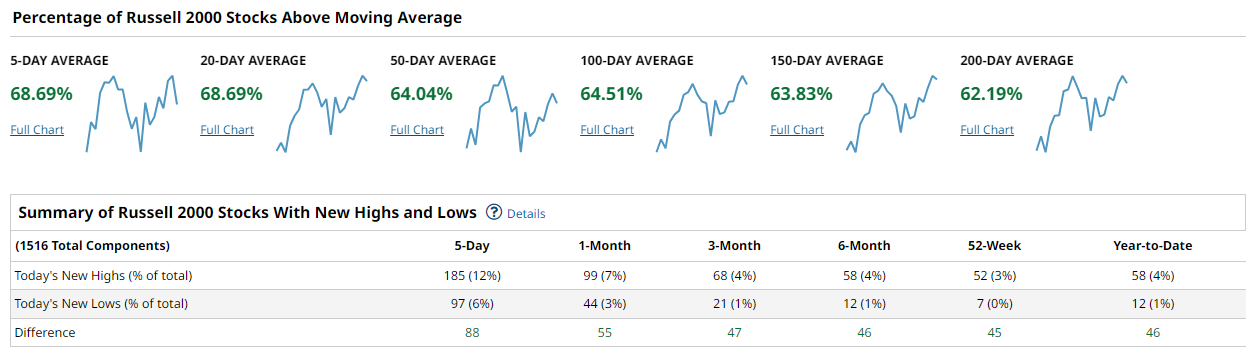

The Russell 2000 continues to play the role of slightly skeptical cousin at the family rally. Price action has improved, but the proportion of small caps above the 50-, 100-, and 200-day averages lags the large-cap complex, and the new-high list is thin relative to new lows across shorter lookbacks.

When small caps do not fully confirm, you usually have a tradable trend in large caps, but the “everything is booming” regime is not quite here yet.

Put together, cap-weighted indexes look stronger than the broad market, with leadership concentrated in the S&P and Nasdaq megacaps while participation in smaller names and slower-moving Dow constituents is positive but not explosive. A more durable advance would be confirmed by seeing 50-day cohorts across all four indexes push clearly above roughly two-thirds of constituents, alongside a clear edge of new highs over new lows for several weeks in a row.

Playbook so far this week: lean bullish but not bravado-bullish. Favor quality large caps and the sectors already showing both strong weekly returns and solid breadth, while avoiding the weakest small-cap pockets that remain below their intermediate averages. Watch for follow-through in 50-day breadth and a cleaner domination of new highs over new lows as your confirmation that this is an advance to press.

Bottom line: this looks like a real uptrend with incomplete participation, worth riding but still worth actively managing risk.